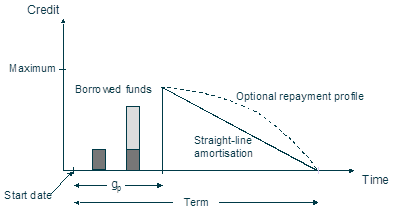

A typical debt facility has a fixed term (defined as a Start Date

plus n year Term) within which funds may be borrowed, up to an optional credit limit (defined by the Maximum Credit input: the default value of 0.0 means that there is no limit to the borrowing offered). Separate Grace Periods are allowed for the principal repayment or amortisation (gp) and the interest payments (gi). New borrowing is only allowed up to gp where gp ≥ gi.

After the principal grace period, amortisation may be paid in one or more equal annual instalments (straight-line amortisation), or there may be an optional repayment profile.

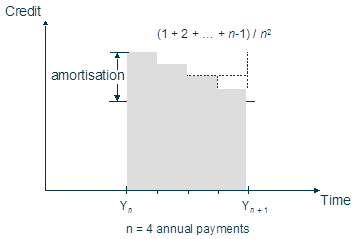

There is typically a fixed Interest Rate for the term, with payments calculated from the year-beginning balance. Small adjustments are made for the interim amortisation: a.(n – 1) / 2n, where a = annual amortisation, and n = number of payments each year:

Variable-rate loans

can be handled by defining the interest rate as a time series: for example, external bank rate + x%.

Other fee structures are also possible:

- up-front fixed fee at the start of the term (Fixed Start input)

- up-front variable fee as a percentage of the new credit each year (Variable Start Prop. input)

- yearly fixed administrative fee (Fixed Annual input)

- yearly variable fee as percentage of unused credit (where a maximum is defined) (Variable Annual Prop. input).

All fees are charged as annual expenses.

Bonds and working capital facilities

A bond is a one-off loan over a fixed period, borrowing x and repaying y, typically with y > x and usually with interest charged as well. This is like an indefinite repayment grace period, but with a fixed one-off amount (see the section below on Sourcing incremental borrowing). Bonds may be traded between creditors, but this has no impact on the borrower’s liability.

It is usual for an operator to have a pre-arranged working capital facility. This is a fully-flexible debt facility (borrow/payback) with interest, and usually with a limited credit facility. This might be captured as a renewable facility with a one-year term.

Sourcing incremental borrowing

When an operator borrows incrementally from a number of facilities, this can occur in two ways. One option is for each facility to specify a

Mapping

to define what share of the incremental borrowing it should satisfy. Any facility with a credit limit already – or becoming – fully subscribed withdraws from this allocation.

Additionally, facilities may specify a Sequence Index that determines the order in which they are used, only proceeding to a higher-index facility (or group of facilities) when the first is fully subscribed.

Residual borrowing and repayment

Borrowing over and above the defined credit facilities and limits is assumed to be covered by a fully flexible instrument identified with the existing global Borrowing Rate input. If required, borrowing reduces ahead of the scheduled amortisation on fixed instruments; there will then be a correlating surplus cash.

Further refinements

Borrowing made in separate tranches may have associated creditor (repayment) classes. However, this is only relevant in the case of bankruptcy, which is beyond the required scope.

A commercial facility might include covenants or conditions for drawing down further capital. A simple example would be for credit to be contingent on EBITDA in previous quarter. However, these might refer to very specific sub-network results, or use quite arbitrary formula, so verifying such conditions is currently left as an exercise for the modeller.